A job relocation home sale is a company-supported process that helps employees sell their primary residence quickly and efficiently when moving for a new job, typically coordinated by relocation management companies (RMCs) to reduce financial disruption. The industry term for this broader process is "employer-assisted home sale," and it covers several structured programs designed to protect employees from double housing costs, tax burdens, and market timing risk. The most widely used of these programs is the Buyer Value Option (BVO), which structures the transaction to preserve tax efficiency for both employer and employee. Understanding how these programs work, what they cover, and where the risks lie gives you a real advantage when negotiating your relocation package.

What is job relocation home sale and how does it work?

A job relocation home sale is a corporate-supported mechanism where the employer, often through a third-party RMC, coordinates the sale of an employee's home as part of a job transfer package. The goal is straightforward: get the employee to their new location without leaving them stuck paying two mortgages or absorbing a loss from a rushed sale. RMCs like Cartus, SIRVA, and Graebel handle the logistics, from listing coordination to closing paperwork, so the employee can focus on starting the new role.

The process typically begins when the employer activates a relocation benefit after a job offer is accepted. The employee receives a relocation package that may include home sale assistance, moving cost coverage, and temporary housing. From there, the RMC steps in to manage the home sale timeline, often setting a defined marketing period before triggering additional support options. This structure exists because uncoordinated home sales during relocations frequently result in delayed starts, financial strain, and employee dissatisfaction.

How does the Buyer Value Option program work?

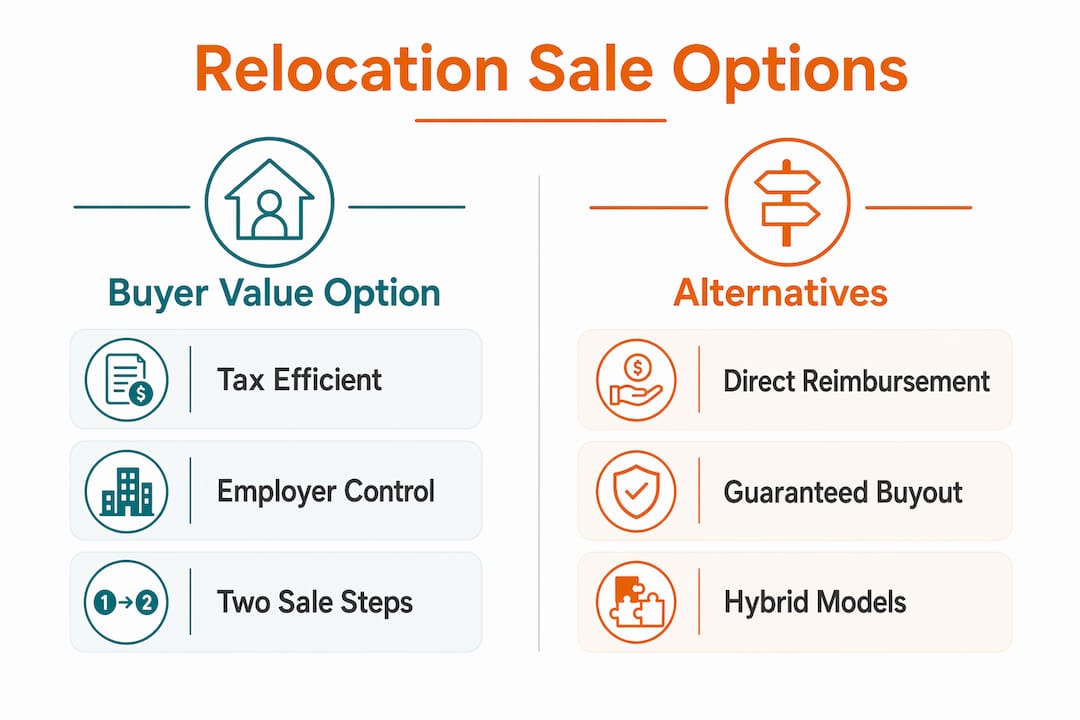

The Buyer Value Option (BVO) is the most common structured program in employer-assisted home sales, and it works through a deliberate two-step transaction designed to eliminate taxable income for the employee. Here is how the process unfolds:

- Employee markets the home. You list your property and find a qualified outside buyer on your own or with a real estate agent. The RMC sets a marketing period, typically 60 to 90 days, during which you work to secure an offer.

- RMC reviews and approves the offer. Once you have a bona fide offer, the RMC evaluates it. If it meets program criteria, the RMC agrees to purchase the home from you at the negotiated price.

- RMC buys from the employee. The RMC purchases your home directly, taking on beneficial ownership and the financial risk of the property between the two closings.

- RMC resells to the outside buyer. The RMC then completes the second transaction, selling the property to the outside buyer you originally found.

- Employee receives proceeds. You receive your sale proceeds from the RMC, not from the outside buyer, which is the structural key to the tax benefit.

This two-sale structure means the home sale assistance is treated as a business transaction rather than compensation to you. As a result, BVO programs reduce the need for tax gross-ups and prevent the assistance from appearing as taxable income on your W-2. For a home sale involving $30,000 or more in employer assistance, that distinction can save thousands of dollars.

One critical rule: you cannot sign directly with the outside buyer at any point. All contracts must flow through the RMC. Bypassing this step collapses the two-sale structure and disqualifies the tax treatment entirely.

Pro Tip: Ask your employer's RMC for a written program summary before listing your home. Knowing the exact marketing period, minimum offer thresholds, and contract routing requirements prevents costly mistakes that could void your tax benefits.

How do BVO alternatives compare for relocation home sales?

Not every employer offers a BVO program. Several alternative models exist, and each carries different levels of risk, tax exposure, and employer cost. Understanding the differences helps you negotiate a better package.

Direct reimbursement is the simplest model. Your employer reimburses you for selling costs such as agent commissions and closing fees after the sale closes. The problem is that reimbursement is treated as taxable income to you, which means you may owe federal and state income tax on the assistance received. Employers often add a tax gross-up payment to cover this burden, but the gross-up itself can also be taxable, creating a compounding cost problem.

Relocation home buyout (also called a Guaranteed Buyout or GBO) means the company buys your home at an independently appraised value, regardless of whether an outside buyer has been found. This gives you certainty and speed, but it shifts significant financial risk to the employer. Because of that cost, GBO programs are less common for mid-level employees and more frequently reserved for senior executives.

Hybrid programs are increasingly standard. Employers typically start with a BVO period to let the market work, then offer a guaranteed buyout as a backstop if the home does not sell within the marketing window. This balances your peace of mind against the employer's budget.

| Program | Tax risk to employee | Employee finds buyer? | Employer cost |

|---|---|---|---|

| Buyer Value Option (BVO) | Low (structured sale) | Yes | Moderate |

| Direct reimbursement | High (taxable income) | Yes | Low |

| Guaranteed buyout (GBO) | Low | No | High |

| Hybrid BVO + GBO | Low | Yes, then no | Moderate to high |

The right model depends on your home's market, your timeline, and what your employer is willing to fund. Always ask whether the program includes a GBO backstop before you accept a relocation offer.

What are the tax implications of a relocation home sale?

Tax treatment is where most employees get surprised during the job relocation process, and the surprises are rarely pleasant. The core issue is this: if your employer pays you money to help with your home sale and that payment is not structured through a qualifying program, the IRS treats it as compensation. You owe income tax on it.

Strict documentation and a two-contract structure are required to maintain the tax efficiency of a BVO program. The IRS has specific guidance on this, and audits of corporate relocation programs do occur. Failing to maintain audit-ready files, or allowing the employee to sign directly with the outside buyer, disqualifies the favorable tax treatment and can result in significant back taxes for both the employee and the employer.

Key documentation requirements include:

- Separate purchase contracts between employee and RMC, and between RMC and outside buyer

- Evidence that the RMC held beneficial ownership between the two closings

- No direct financial exchange between employee and outside buyer

- Written program approval from the employer before listing

Pro Tip: Keep a dedicated folder with every email, contract, and closing document related to your relocation home sale. If the IRS questions the transaction structure years later, your paper trail is your only defense.

Understanding the costs involved in selling your home matters here too. Even in a well-structured BVO program, some expenses may fall outside the covered benefits, and knowing what you owe out of pocket prevents budget surprises at closing.

How to prepare for selling your home during a job relocation

Preparation separates employees who close smoothly from those who scramble. The job transfer home sale process has hard deadlines tied to your start date, and delays in the home sale cascade directly into your work life.

- Request your relocation package in writing before accepting the offer. Verbal commitments about home sale assistance are unenforceable. Get the full program details, including marketing period length, covered costs, and GBO availability, documented before you sign anything.

- Contact the RMC immediately after accepting. Relocation teams handle timelines and pay relocation-related real estate and closing costs, but only if you engage them early. Waiting weeks to make contact compresses your marketing window and limits your options.

- Price your home accurately from day one. Overpricing during a relocation sale is a common and costly mistake. You have a fixed marketing window. A home that sits for 45 days and then requires a price cut often sells for less than a correctly priced home listed on day one.

- Budget for costs outside the relocation package. Negotiating relocation packages and getting agreements in writing protects you, but no package covers everything. Factor in overlap costs, storage, and temporary housing into your personal budget.

- Understand the escrow timeline. The escrow process in a relocation sale can differ from a standard transaction because the RMC is the legal seller in the second contract. Know who holds escrow and what triggers the release of your proceeds.

Timing your listing to align with your job start date is the single most controllable variable in this process. If your start date is firm, work backward from it to set your listing date, marketing period, and target closing date.

Key takeaways

A properly structured employer-assisted home sale protects employees from taxable income, double housing costs, and market timing risk, but only when the correct program and documentation are in place.

| Point | Details |

|---|---|

| BVO is the most tax-efficient model | The two-sale structure prevents home sale assistance from becoming taxable income for the employee. |

| Documentation is non-negotiable | Audit-ready files and separate contracts are required to preserve IRS-compliant tax treatment. |

| GBO provides certainty at higher cost | A guaranteed buyout removes market risk for the employee but increases employer financial exposure. |

| Early RMC engagement is critical | Contacting the relocation management company immediately after accepting the offer protects your marketing window. |

| Get everything in writing | Verbal relocation package commitments are unenforceable; written agreements prevent costly disputes. |

What I've learned from watching relocation sales go wrong

I've seen homeowners in Northwest Indiana accept relocation packages without reading the fine print, and the results are predictable. They miss the marketing window, the GBO backstop isn't available, and they end up selling under pressure at a price that doesn't reflect what their home is worth.

The most underrated step in the entire job relocation process is the conversation you have with your employer before you accept the offer. Most employees treat the relocation package as a fixed benefit. It isn't. Companies negotiate these terms regularly, and employees who ask specific questions about BVO availability, marketing periods, and covered closing costs consistently get better outcomes than those who accept the standard offer without pushback.

The other thing I'd tell any homeowner facing a relocation sale: your timeline is your biggest risk factor. The real estate market in Northwest Indiana moves at its own pace, and a home that needs work before it can list competitively is a liability when you have a 60-day marketing window. If your home has deferred maintenance, an outdated kitchen, or any condition issue that would slow a traditional sale, you need to factor that into your decision about whether to go through the RMC program or pursue a faster alternative.

Relocation sales also carry an emotional weight that people underestimate. You are selling the place where your family lived while simultaneously starting a new job in a new city. The stress compounds. Having a clear plan, a realistic timeline, and a trusted local contact who knows the market makes a measurable difference in how the process feels and how it ends.

— Daniel

Sell your home fast in Northwest Indiana with Nwibuyers

Relocating for work in Northwest Indiana and need to sell quickly without the uncertainty of a traditional listing? Nwibuyers purchases homes directly for cash in Hammond, Highland, Hobart, and Crown Point, with no repairs required and no open houses. The process at Nwibuyers is built for exactly this situation: a fair cash offer, a closing timeline that fits your move, and zero fees or commissions eating into your proceeds. Some sellers close in as few as five days. If your relocation package doesn't include a guaranteed buyout or your marketing window is running short, sell your house fast in Hammond or the surrounding area directly through Nwibuyers and move forward with confidence.

FAQ

What is a job relocation home sale?

A job relocation home sale is an employer-supported process that helps employees sell their primary residence when moving for a new job, typically managed by a relocation management company to reduce financial and logistical burden.

What is the Buyer Value Option in relocation?

The Buyer Value Option (BVO) is a two-step home sale structure where the employee finds a buyer, the RMC purchases the home from the employee, and then resells it to that buyer. This structure prevents the sale assistance from becoming taxable income to the employee.

Does relocation home sale assistance count as taxable income?

It depends on the program structure. Direct reimbursement is treated as taxable income, while properly structured BVO programs avoid this by routing the transaction through the RMC as a business sale rather than employee compensation.

What happens if my home doesn't sell during the relocation marketing period?

Many employers offer a guaranteed buyout as a backstop after the BVO marketing period expires. The company purchases the home at an appraised value, giving the employee a guaranteed sale regardless of market conditions.

Can I sell my home directly without going through the relocation company?

Yes, but doing so typically means forfeiting employer-assisted home sale benefits. Homeowners who need speed and certainty outside of a corporate program often work with cash buyers like Nwibuyers to close quickly without repairs or agent fees.