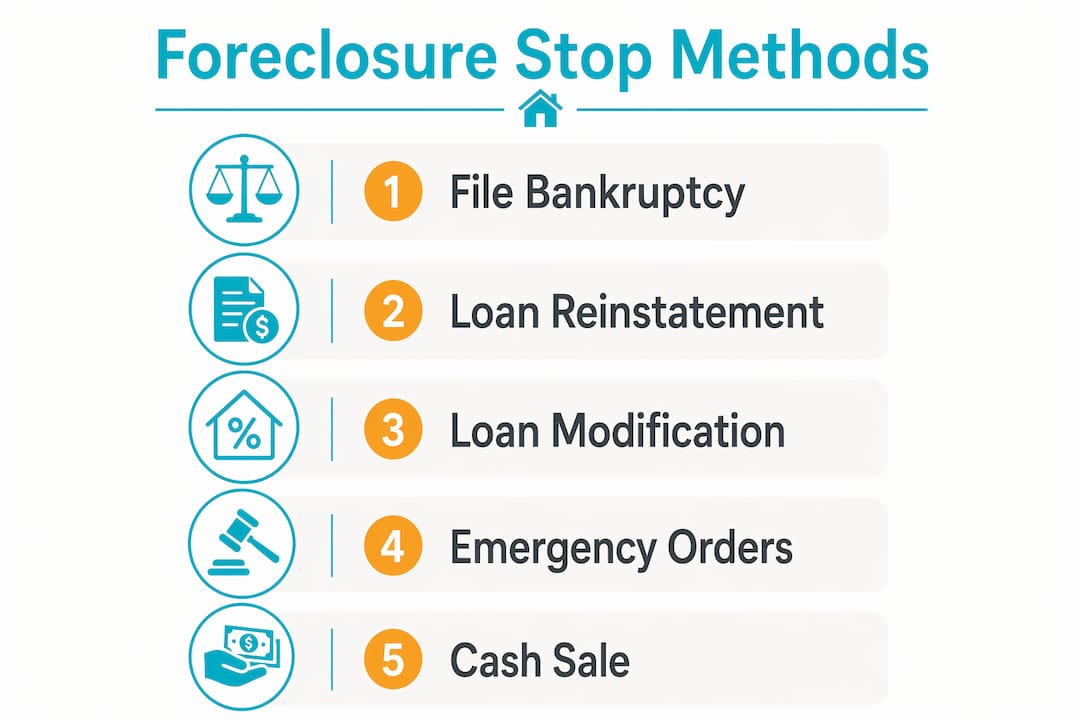

Stopping a foreclosure sale fast is defined as using immediate legal or financial tools to halt a scheduled auction before your home transfers to a new owner. The bankruptcy automatic stay, loan reinstatement, Regulation X loss mitigation protections, temporary restraining orders (TROs), and HUD-approved housing counseling are the five methods that can interrupt a foreclosure sale, sometimes within hours. Timing is everything. Each method has a hard deadline, and missing it by even one day can cost you your home. This guide breaks down exactly how each option works, what it costs, and when to use it.

How to stop foreclosure sale fast with bankruptcy

Bankruptcy is the fastest lever available to homeowners facing a sale scheduled within days. The moment you file, a federal automatic stay takes effect under 11 U.S.C. § 362, which stops foreclosure activity immediately, pending court approval. No phone call, no negotiation, no lender agreement required. The filing itself is the trigger.

Chapter 7 vs. Chapter 13: which one actually saves your home

Chapter 7 and Chapter 13 serve different purposes in a foreclosure crisis. Chapter 7 liquidates unsecured debt and buys you time, typically 30 to 90 days, but it does not let you catch up on missed mortgage payments. Chapter 13 is the option that can actually save your home long term because it allows you to repay arrears over a three to five year repayment plan while keeping current on future payments.

The cost difference matters when you are moving fast. The Chapter 7 filing fee is $338, while Chapter 13 attorney fees typically range from $2,500 to $7,000. Many bankruptcy attorneys allow those fees to be folded into the repayment plan, which means you do not need the full amount upfront to file. That detail alone removes the biggest barrier most homeowners face when time is short.

One critical limitation: if you have filed bankruptcy before and the court dismissed your case within the past year, the automatic stay may only last 30 days or may not apply at all. Your attorney must file a motion to extend it. Lenders can also file a motion for relief from the stay, which, if granted, allows them to resume foreclosure proceedings. Choosing the right chapter and timing your repayment plan correctly is what separates a temporary delay from a real solution.

- File as early in the day as possible on the day before the scheduled sale

- Bring proof of filing to the courthouse or auction site if needed

- Notify your mortgage servicer immediately after filing

- Work with a bankruptcy attorney who has same-day or emergency filing experience

Pro Tip: Fax or email your bankruptcy case number directly to the foreclosing attorney's office the moment you receive it. Servicers and foreclosure attorneys sometimes proceed with a sale if they have not received official notice, even when the stay is technically in effect.

Can reinstatement or loan modification stop the sale in time?

Reinstatement is the most straightforward way to halt foreclosure proceedings fast without involving a court. Reinstatement stops foreclosure by requiring a single lump-sum payment covering all missed mortgage payments, late fees, attorney fees, and any other costs the servicer has accrued. Once that payment is received and processed, the loan returns to current status and the sale is canceled.

The challenge is the deadline. Most states require reinstatement to occur a set number of days before the scheduled sale, and that window varies by state law and your loan documents. Indiana homeowners should confirm their reinstatement deadline directly with their servicer and request a written payoff figure. That written figure locks the amount and gives you a paper trail.

Loan modification and forbearance take a different path. Instead of paying everything at once, you apply for a change to your loan terms. The protection here comes from federal law. Under Regulation X, 12 CFR § 1024.41, a servicer cannot proceed with a foreclosure sale while evaluating a complete loss mitigation application submitted more than 37 days before the scheduled sale. That 37-day rule is your legal shield, but only if your application is complete.

Here is what a complete application typically requires:

- Completed borrower assistance form (provided by your servicer)

- Two most recent pay stubs or proof of income

- Two most recent federal tax returns

- Two most recent bank statements for all accounts

- Hardship letter explaining the reason for default

- Proof of any other income such as Social Security or rental income

| Document | Why it matters |

|---|---|

| Hardship letter | Establishes eligibility for loss mitigation programs |

| Proof of income | Determines which modification options you qualify for |

| Bank statements | Verifies financial position and ability to repay |

| Tax returns | Confirms income consistency over time |

The completeness and timing of your application determine whether federal protections apply. A partial application does not trigger the 37-day rule. Servicers are required to notify you of missing documents within five business days, so submit early and follow up in writing every time.

Pro Tip: Send your loss mitigation application via certified mail and keep the return receipt. Servicers have been known to dispute the receipt date, and your certified mail timestamp is the evidence that triggers the federal protection clock.

What are emergency court orders and when do they work?

A temporary restraining order (TRO) is a court-issued emergency order that can stop a foreclosure auction immediately when there is evidence of a legal defect in the foreclosure process. Courts can grant TROs on very short notice, sometimes within hours, but only when you can demonstrate a specific procedural violation or legal error.

The types of defects that support a TRO include:

- Improper or defective notice of the foreclosure sale

- Fraud or misrepresentation by the lender or servicer

- Dual tracking violations, where the servicer continued foreclosure while evaluating your loss mitigation application

- Failure to follow state-mandated foreclosure procedures

- Errors in the chain of title or loan ownership documentation

Emergency motions like TROs require a tight factual record, especially when the sale is imminent. You need an attorney who can file the motion, draft a supporting affidavit, and appear before a judge on the same day. Courts do not grant TROs based on financial hardship alone. The legal defect must be documented and credible.

A TRO is most effective when combined with another strategy. For example, if your servicer violated the dual tracking prohibition under Regulation X while you had a pending modification application, that violation supports both a TRO and a federal complaint to the Consumer Financial Protection Bureau (CFPB). Using both simultaneously creates pressure from two directions at once.

How does HUD counseling help you prevent foreclosure quickly?

HUD-approved housing counseling offers free, confidential assistance to homeowners facing foreclosure. HUD-certified counselors help you understand every loss mitigation option available, assemble the required documentation, and communicate directly with your servicer on your behalf. That last point matters more than most homeowners realize.

Servicers respond differently when a HUD counselor is involved. Counselors know the internal escalation paths, the correct department contacts, and the regulatory requirements servicers must follow. Early contact with HUD counselors improves your chances of assembling a complete loss mitigation application the first time, which is the single biggest factor in whether federal delay protections apply.

You can reach the HUD HOPE Hotline at 1-800-569-4287. The service is free, available in multiple languages, and connects you with a local agency that knows your state's specific foreclosure timeline and laws.

Watch for these warning signs of foreclosure rescue scams:

- Anyone who asks you to sign over the deed to your home

- Companies that promise to stop foreclosure for an upfront fee before doing any work

- Advisors who tell you to stop communicating with your lender or servicer

- Offers that seem too good to be true, such as guaranteed loan modifications

Homeowners should not fight foreclosure alone. The combination of a HUD counselor and a foreclosure attorney gives you the strongest possible position, especially when a sale date is already scheduled. You can also review foreclosure options in Indiana to understand what local resources and alternatives are available to you.

Key takeaways

Stopping a foreclosure sale fast requires using the right legal or financial tool before the sale date, with bankruptcy providing the fastest protection and loss mitigation applications providing the strongest federal shield when submitted more than 37 days in advance.

| Point | Details |

|---|---|

| Bankruptcy automatic stay | Filing triggers an immediate federal halt to foreclosure activity under 11 U.S.C. § 362. |

| 37-day Regulation X rule | A complete loss mitigation application submitted 37+ days before sale legally blocks the servicer from proceeding. |

| Reinstatement deadline | Paying all arrears in a lump sum before the state deadline cancels the sale and restores current loan status. |

| TRO requirements | Emergency court orders require documented legal defects, not just financial hardship, to succeed. |

| HUD counseling | Free HUD-approved counselors improve application completeness and servicer response, at no cost to you. |

What I have learned after years of watching homeowners face this crisis

The homeowners who stop foreclosure sales fast share one trait: they act before they feel ready. The ones who lose their homes almost always waited for a perfect plan that never came. I have seen people with strong cases lose their homes because they spent three weeks researching instead of filing.

Bankruptcy gets a bad reputation, but for someone with a sale scheduled in 48 hours, it is not a financial failure. It is a legal tool, and using it correctly buys time to pursue a real solution. Chapter 13 in particular is underused by homeowners who assume they cannot afford it, not realizing attorney fees can be paid through the repayment plan itself.

The other mistake I see constantly is submitting an incomplete loss mitigation application. Homeowners send in what they have and assume the servicer will ask for the rest. Servicers are not your advocates. They will process an incomplete application, deny it for incompleteness, and continue the foreclosure timeline. The 37-day federal protection only activates on a complete application. That word carries legal weight.

If you are in Northwest Indiana and the sale is close, selling to a cash buyer is a legitimate strategy that stops foreclosure immediately by paying off the loan before the auction. It is not giving up. It is taking control of the outcome on your terms rather than the bank's. Explore how cash buyers work before you assume it is not an option for your situation.

— Daniel

Dan buys houses can stop your foreclosure fast with a cash offer

If the sale date is close and the legal options feel overwhelming, selling your home for cash is one of the fastest ways to stop home foreclosure before the auction happens. Dan buys houses purchases homes in Northwest Indiana in any condition, with no repairs, no open houses, and no lengthy negotiations required.

Some sellers close in as little as five days, which is fast enough to pay off the mortgage balance and stop the foreclosure process entirely. There are no fees, no commissions, and no pressure. Dan buys houses gives you a straightforward cash offer so you can make a clear decision under a tight deadline. Get a cash offer today and find out exactly what your home is worth before the sale date arrives.

FAQ

How fast can bankruptcy stop a foreclosure sale?

Bankruptcy stops a foreclosure sale the moment the petition is filed, triggering an automatic stay under federal law that halts all creditor collection activity including scheduled auctions. Filing even one day before the sale can legally prevent it from proceeding.

What is the 37-day rule for loan modifications?

Under Regulation X, a servicer cannot proceed with a foreclosure sale while evaluating a complete loss mitigation application submitted more than 37 days before the scheduled sale date. The application must be complete, meaning all required documents are received and acknowledged by the servicer.

Can I stop foreclosure without filing bankruptcy?

Yes. Reinstatement, a complete loan modification application, a temporary restraining order, or a cash sale can each stop a foreclosure sale without bankruptcy. The right option depends on how much time you have before the scheduled sale and your financial situation.

What makes a TRO different from other foreclosure stops?

A TRO requires proof of a specific legal defect in the foreclosure process, such as improper notice or dual tracking violations, rather than financial hardship. It is a court order granted on an emergency basis and is most effective when combined with a federal complaint to the CFPB.

Is HUD counseling really free?

HUD-approved housing counseling is free and confidential for homeowners facing foreclosure. You can access it through the HUD HOPE Hotline at 1-800-569-4287, which connects you with a local agency that can help you apply for loss mitigation programs and communicate with your servicer.