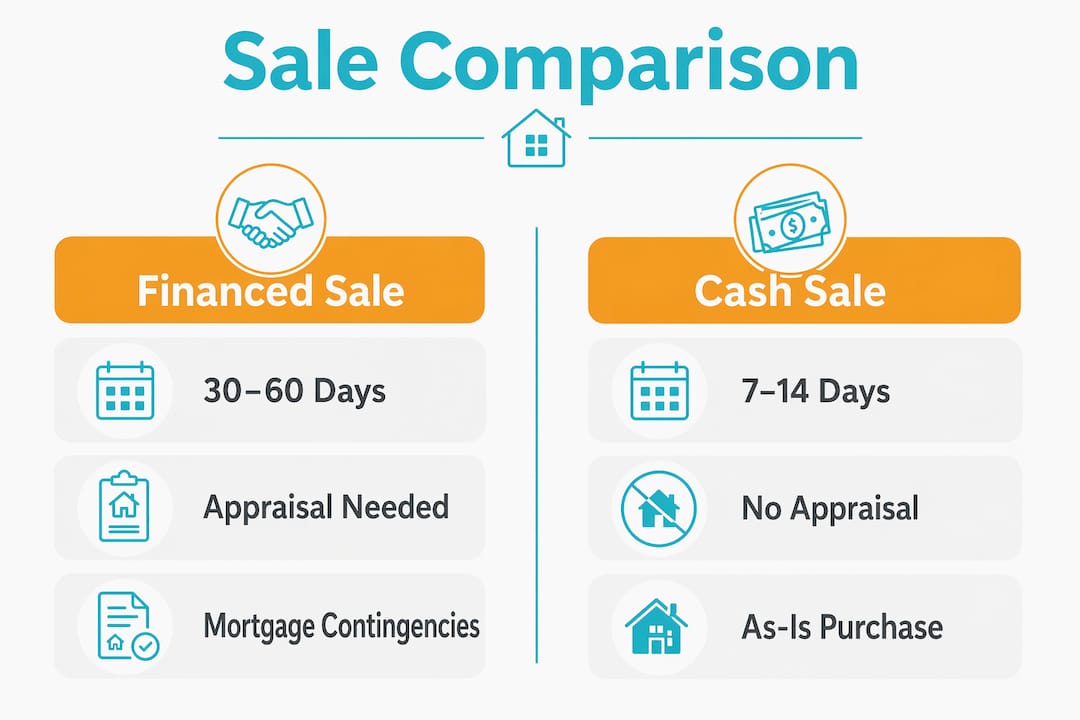

Cash buyers close home sales faster than financed buyers by removing every mortgage-related step that causes delays in a traditional transaction. Where a financed sale typically takes 30–60 days, a cash sale can close in as few as 7–14 days. That speed is not a marketing claim. It reflects the structural difference between a buyer who brings their own funds and one who depends on a lender, an underwriter, an appraiser, and a loan officer to approve the deal. For homeowners facing foreclosure, relocation, or an inherited property they need to move quickly, understanding why cash buyers close faster is the difference between a stressful sale and a clean exit.

Why cash buyers close faster: the mechanics behind the speed

The speed of cash transactions comes down to one thing: no lender in the deal. When a buyer finances a home, the lender controls the timeline. The lender orders an appraisal, assigns an underwriter, reviews the buyer's income and credit history, and issues a loan commitment letter. Each of those steps takes time, and none of them are in your control as the seller.

Cash buyers avoid the 30–45 day window that lender appraisal and loan approval processes typically consume. That single fact explains most of the speed advantage. No appraisal means no waiting for a licensed appraiser to schedule a visit, complete a report, and submit it to the lender for review. No underwriting means no back-and-forth requests for additional documents that can stall a deal for weeks.

The process also cuts out mortgage contingencies. In a financed sale, the buyer's offer is conditional on securing a loan. If the loan falls through, the deal collapses. Cash offers carry no such condition. The buyer has the funds. The transaction moves directly from accepted offer to title search, closing disclosure, and settlement.

Pro Tip: Ask any cash buyer upfront for proof of funds before you accept their offer. A legitimate cash buyer will provide a bank statement or letter from a financial institution without hesitation. This one step protects you from buyers who claim to be cash buyers but are not.

What steps remain in a cash sale

Cash sales are not entirely free of process. Title searches still happen. Closing disclosures still get prepared. Some cash buyers request a voluntary inspection before finalizing the purchase. The difference is that none of these steps involve a third-party lender, so they move on the buyer's schedule rather than a bank's. A title search that might take a week in a cash deal can be held up for days waiting on lender requirements in a financed one.

How does market timing affect the benefits of a fast cash closing?

The speed advantage of cash buyers matters most in the first four weeks a home sits on the market. The first four weeks are the critical window when sellers hold the most pricing leverage and attract the most serious buyers. After that window closes, listings start to feel stale, and buyers begin to wonder what is wrong with the property.

Nationally, 18.5% of homes go pending within seven days, and in competitive markets like St. Louis and Seattle, one in three homes sells within a week and attracts bidding wars. That data shows how quickly the market separates motivated sellers from those who wait. In spring and early summer, the median listing time sits at around 31 days, with prices running 16% higher than slower months. Miss that window, and you are selling into a weaker position.

Here is what extended time on market actually costs you:

- Price cuts become likely. Homes that linger past the initial listing period lose leverage and often require price reductions to attract renewed interest.

- Buyer perception shifts. A listing that has been sitting for weeks signals to buyers that something may be wrong, even when nothing is.

- Negotiating power drops. The longer your home sits, the more a buyer feels entitled to ask for repairs, credits, and concessions.

- Carrying costs add up. Every additional month means another mortgage payment, insurance bill, and utility cost you absorb.

Cash buyers act within that critical four-week window. They do not need to wait for loan approval before making a firm offer. That speed protects your pricing position and keeps you from sliding into the stale listing trap.

What are the practical advantages of cash offers beyond speed?

Speed is the headline, but the practical benefits of cash offers go further. Convenience is the primary value cash offers deliver to sellers. Removing the human dependencies in a financed deal, such as underwriters, loan officers, and appraisers, eliminates the most common sources of last-minute deal collapse.

The table below compares what a traditional financed sale looks like against a cash sale for a seller who needs to move quickly.

| Factor | Financed sale | Cash sale |

|---|---|---|

| Closing timeline | 30–60 days | 7–14 days |

| Appraisal required | Yes, lender-ordered | No |

| Loan contingency | Yes | No |

| Risk of deal collapse | Higher (loan denial) | Lower |

| Repair negotiations | Common | Rare or none |

| Renovation required | Often expected | Typically not |

| Open houses needed | Usually | No |

For homeowners who have inherited a property, are facing foreclosure, or need to relocate for work, every one of those rows matters. You are not just saving time. You are removing the uncertainty that makes a traditional sale so stressful.

Cash buyers also tend to purchase homes as-is. That means you do not need to repaint, replace appliances, or fix the roof before listing. If you want to understand what conditions cash buyers accept, the range is wider than most sellers expect. Structural issues, deferred maintenance, and cosmetic problems that would scare off a financed buyer are often acceptable to a cash buyer who plans to renovate after purchase.

Pro Tip: Do not assume a lower cash offer is automatically a bad deal. Factor in what you would spend on repairs, agent commissions, and carrying costs during a longer traditional sale. The net difference is often smaller than the headline numbers suggest.

What should homeowners know about cash sale misconceptions?

The biggest misconception about cash sales is that they involve no due diligence. That is not accurate. Cash buyers may still request voluntary inspections, and sellers often mistake those inspection requests for financing contingencies. They are not the same thing.

Here is what actually changes in a cash sale versus what stays the same:

- What changes: No lender appraisal, no loan approval waiting period, no mortgage contingency, no underwriting review.

- What may stay: A voluntary inspection, a title search, a due diligence period negotiated between buyer and seller.

- What sellers sometimes misread: A cash buyer requesting an inspection is not the same as a buyer with a financing contingency. The cash buyer can still close without the inspection results forcing a lender's hand.

The due diligence period in a cash deal is typically shorter than in a financed one because the buyer is not waiting on a third party to approve the transaction. A cash buyer who wants a 10-day inspection window can complete that review and still close faster than a financed buyer who needs 45 days just for loan processing.

Sellers should also know that cash buyers can and do negotiate. A cash offer is not automatically a take-it-or-leave-it situation. Price, closing date, and which party covers closing costs are all negotiable. The advantage is that once you agree on terms, the deal is far less likely to fall apart. For more on selling an estate home quickly, the process shares many of the same principles.

Key takeaways

Cash sales close faster because they remove lender-controlled steps, and that speed directly protects a seller's pricing leverage, certainty, and net proceeds.

| Point | Details |

|---|---|

| No lender means faster closing | Cash buyers skip appraisal, underwriting, and loan approval, cutting weeks from the timeline. |

| First four weeks are critical | Sellers hold the most pricing power in the first month; cash buyers act within that window. |

| As-is sales reduce seller burden | Cash buyers typically purchase without requiring repairs or renovations before closing. |

| Inspections still happen | Cash buyers may request voluntary inspections, but these do not involve lender approval delays. |

| Net proceeds often compare favorably | After repairs, commissions, and carrying costs, cash offers frequently match or beat financed sale net returns. |

What I have learned about matching seller urgency to buyer type

I have worked with homeowners in Northwest Indiana who waited three months for a financed deal to close, only to watch it collapse two weeks before settlement because the buyer's loan was denied. That experience is more common than most sellers expect, and it is devastating when you are already under financial pressure.

The sellers who come out ahead are the ones who recognize their situation clearly. If you have time, a traditional sale with a financed buyer might get you a higher headline price. But if you are facing a foreclosure deadline, a job transfer, or an inherited property you cannot afford to maintain, the math changes completely. The cost of waiting is real, and it compounds every month.

What I find most sellers underestimate is how much the certainty of a cash close is worth. A financed buyer at a higher price is a conditional offer. A cash buyer at a fair price is a done deal. For someone who needs to move on with their life, that certainty has genuine financial value beyond what shows up in the offer number.

The sellers I respect most are the ones who ask the right question: not "which offer is highest?" but "which offer actually closes?" Those two questions have different answers more often than people realize.

— Daniel

Ready to skip the wait and sell on your terms?

If you are facing a situation where time matters, Dan buys houses works with homeowners across Northwest Indiana to make the process straightforward. No repairs, no open houses, no waiting on a bank to approve someone else's loan.

Dan buys houses makes cash offers on homes in any condition, and some sellers close in Hammond in as little as five days. If you want to understand exactly how the process works before you commit to anything, you can review how we buy houses step by step. There is no cost, no obligation, and no pressure. Just a clear offer and a closing date that works for you.

FAQ

Why do cash buyers close so much faster than financed buyers?

Cash buyers skip lender appraisal, underwriting, and loan approval steps that add 30–45 days to a financed transaction. Without a lender in the deal, the sale moves directly from accepted offer to title and settlement.

Do cash buyers still do inspections?

Yes, cash buyers may request voluntary inspections, but these are not financing contingencies. The buyer can still close regardless of what the inspection finds, unlike a financed buyer whose lender may require repairs before approving the loan.

How fast can a cash sale actually close?

Most cash sales close in 7–14 days. In some cases, with clear title and motivated parties, closing can happen in as few as five days. That compares to the 30–60 day standard for financed home sales.

Will I get less money selling to a cash buyer?

A cash offer may carry a lower headline price, but sellers often net a comparable amount after factoring in agent commissions, repair costs, and carrying costs during a longer traditional sale. The certainty of closing also has real financial value.

What types of homes do cash buyers purchase?

Cash buyers typically purchase homes in any condition, including properties with deferred maintenance, structural issues, or cosmetic problems. This makes them a practical option for sellers who cannot or do not want to renovate before selling.