An investor cash offer is a purchase proposal where a buyer uses personal liquid funds to buy a home outright, with no mortgage financing involved. That single difference removes appraisal requirements, underwriting delays, and the ever-present risk of a loan falling through at the last minute. Investors account for roughly one-third of residential real estate sales in the U.S. as of 2026. For homeowners facing foreclosure, dealing with a property that needs major repairs, or simply needing to move fast, understanding what is investor cash offer and how it works can be the difference between a stressful ordeal and a clean exit.

What is an investor cash offer and how does it work?

An investor cash offer is a formal purchase proposal backed by liquid funds, not a mortgage. The industry term for this transaction type is a "direct cash purchase," and it works differently from a conventional sale in nearly every step of the process.

Here is how the process typically unfolds:

- You request an offer. The investor reviews your property details, often without an in-person visit at first. Basic information like address, condition, and your timeline is enough to generate a preliminary number.

- The investor calculates their offer. Investors factor in carrying costs and repair expenses alongside their required profit margin. An offer that looks 10% below market value often reflects the renovation budget the investor is absorbing on your behalf.

- Proof of funds is provided. This step separates legitimate buyers from tire-kickers. An official bank statement or a verified letter from a financial institution provides far more deal security than a generic proof-of-funds document.

- Inspections and appraisals are typically waived. Because the investor is buying as-is, the standard contingencies that slow down financed deals are removed. You do not need to fix a leaking roof or update outdated electrical before closing.

- Closing happens fast. Cash transactions close in 10–14 days on average, compared to 30–45 days for financed deals. That speed is not a marketing claim. It reflects the absence of a lender's underwriting queue.

Not all investors operate the same way. House flippers and buy-and-hold investors both purchase with cash but have different business models. Flippers want a quick turnaround after renovation. Buy-and-hold investors plan to rent the property long-term. Both types can close fast, but their offer prices and flexibility may differ.

Pro Tip: Ask every cash buyer for a verified bank statement, not just a letter. Verified statements reduce the risk of a buyer backing out after you have already turned down other offers.

What are the benefits and drawbacks of a cash offer?

The main appeal of a cash offer for distressed or repair-heavy properties is certainty and speed, not the highest possible price. That distinction matters before you sign anything.

Benefits:

- No financing risk. Financing failure is the most common reason sales fall through. A cash buyer eliminates that risk entirely.

- No repairs or staging required. You sell the property in its current condition. There are no contractor bids, no open houses, and no weekend showings to manage.

- Fewer contingencies. iBuyers and direct investors typically waive home inspections and appraisal contingencies, which removes two of the most common deal-killers in traditional sales.

- No agent commissions. Many cash buyers purchase directly, meaning you avoid the standard 5–6% agent commission. Some fees may still apply, so read the contract carefully.

- Speed. Sellers report closing in as little as five days with certain buyers, including Dan buys houses in Northwest Indiana.

Drawbacks:

- Lower offer price. Investors price offers to account for renovation costs, carrying costs, and profit. What seems like a low number is often a fair reflection of the property's as-is condition.

- Less room to negotiate. Investor offers tend to be firm. The trade-off for speed and certainty is less back-and-forth on price.

- Verify buyer reputation. Some cash homebuyer companies charge fees or operate with less transparency. Always check reviews, ask for references, and confirm the buyer's track record before accepting.

"The right question is not 'is this the highest offer?' It is 'does this offer solve my problem?' For sellers facing foreclosure or a property they cannot afford to fix, certainty beats price every time."

How do investor cash offers compare to traditional home sales?

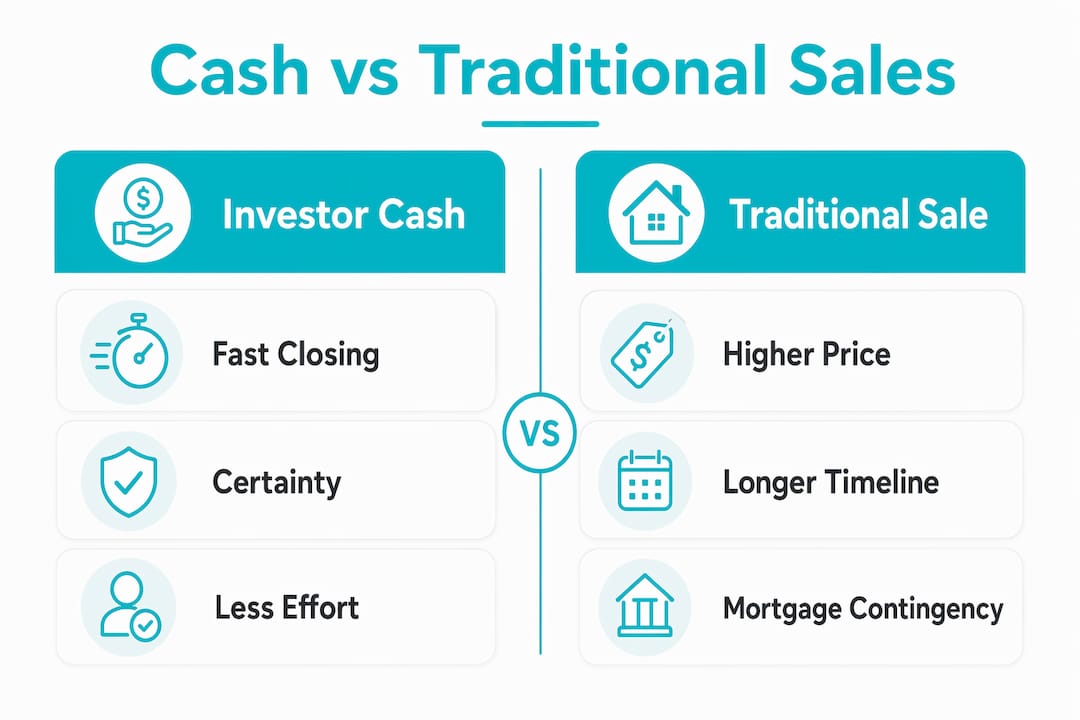

The investor offer vs. traditional sale comparison comes down to four factors: price, timeline, certainty, and effort required from you.

Traditional financed sales involve mortgage approval, a formal appraisal ordered by the lender, and underwriting that can take weeks. A buyer's loan can be denied days before closing, leaving you back at square one. That risk is real, and it falls entirely on the seller.

| Factor | Investor cash offer | Traditional financed sale |

|---|---|---|

| Closing timeline | 10–14 days | 30–45 days |

| Financing risk | None | High (loan denial possible) |

| Repairs required | No | Usually yes |

| Offer price | Below market value | Closer to market value |

| Contingencies | Few or none | Appraisal, inspection, financing |

| Agent commissions | Often none | Typically 5–6% |

| Negotiation flexibility | Limited | More room to negotiate |

Traditional sales can yield a higher final number, but that number is not guaranteed. A financed buyer's offer can collapse at any stage. For homeowners who need to understand the full picture of as-is sales, the gap between a cash offer and a traditional offer often narrows once you subtract repairs, commissions, and carrying costs during a longer listing period.

Sellers in financial distress face a specific risk with traditional sales. Every additional month on the market is another mortgage payment, utility bill, and insurance premium. A cash offer that closes in two weeks can cost less in total than a higher traditional offer that takes three months to close.

When should you accept an investor cash offer?

An investor cash offer fits specific situations well. It is not the right choice for every homeowner, but for the right seller, it is the most practical path available.

Strong indicators that a cash offer makes sense:

- Your property needs significant repairs you cannot afford or do not want to manage.

- You are facing foreclosure and need to close before a court date.

- You have inherited a property in another city and want a clean, fast resolution.

- You are relocating for work and cannot carry two properties simultaneously.

- Your property has been sitting on the market without serious financed offers.

Pro Tip: Before accepting any cash offer, get at least two competing offers from different buyers. Even a second offer you do not accept gives you a benchmark to evaluate whether the first offer is reasonable.

Timing matters too. If you have flexibility, accepting an offer that aligns with your move-out date reduces stress and avoids double moves. Many investors, including Dan buys houses, allow sellers to choose their closing date, which is a practical advantage that rarely gets enough attention.

Verifying legitimacy protects you. Check the buyer's proof of funds carefully and look up their business history. Legitimate cash buyers have a paper trail of completed transactions. Ask for references from past sellers in your area.

Treat the offer as a business decision. Your home has personal value, but an investor's offer reflects the property's condition, local market data, and the investor's cost structure. Sellers who separate emotional attachment from financial reality make better decisions and close with less regret.

For sellers who want to understand what conditions cash buyers accept, the short answer is nearly any condition. Structural issues, outdated systems, fire damage, and code violations are all situations cash investors routinely handle.

Key Takeaways

An investor cash offer is the fastest, most certain path to closing for homeowners who cannot or do not want to repair, stage, or wait out a traditional sale.

| Point | Details |

|---|---|

| Speed of closing | Cash offers close in 10–14 days versus 30–45 days for financed deals. |

| Price trade-off | Lower offers reflect repair costs and investor margin, not an arbitrary discount. |

| Certainty of sale | No financing contingencies means no last-minute deal collapses. |

| Verify the buyer | Always request a verified bank statement, not just a proof-of-funds letter. |

| Best-fit situations | Foreclosure risk, inherited properties, and repair-heavy homes benefit most from cash offers. |

What I have learned after years of buying homes for cash

Most sellers come to me after a difficult experience with a traditional listing. They listed the home, got an offer, and then watched it fall apart when the buyer's loan was denied three weeks before closing. That experience is more common than most real estate agents admit.

The sellers who do best with cash offers are the ones who treat the transaction as a business decision from day one. They get multiple offers, they verify proof of funds, and they calculate the true net after repairs, commissions, and carrying costs. When you run those numbers honestly, the gap between a cash offer and a traditional offer is almost always smaller than it first appears.

The sellers who struggle are the ones who anchor on the highest possible number without accounting for the risk and cost of getting there. A traditional buyer offering $30,000 more than my cash offer sounds better on paper. But if that buyer needs three months to close, requires $15,000 in repairs as a condition of their loan, and has a 20% chance of financing falling through, the math changes quickly.

My honest advice: if your property needs work and you need to move on with your life, a cash offer is not a consolation prize. It is a tool that solves a specific problem efficiently. Use it when it fits. Push back when it does not. And always, always verify who you are dealing with before you sign.

— Daniel

Sell your home fast with Dan buys houses

Homeowners in Northwest Indiana who need a fast, no-repair sale have a direct option with Dan buys houses.

Dan buys houses purchases properties in any condition across Hammond, Highland, Hobart, and the surrounding area. There are no open houses, no contractor visits, and no agent commissions. The process is straightforward: you share your property details, receive a fair cash offer, and choose your closing date. Some sellers close in as little as five days. Whether you are facing foreclosure, dealing with an inherited property, or simply done with a house that needs more work than it is worth, Dan buys houses makes the process clear and fast. Get your offer today at nwibuyers.com/sell-your-house or check availability for Hammond homeowners ready to close quickly.

FAQ

What is an investor cash offer in real estate?

An investor cash offer is a purchase proposal where a buyer uses personal liquid funds to buy a home outright, with no mortgage involved. This removes appraisal and underwriting requirements, allowing for faster and more certain closings.

How fast does an investor cash offer close?

Cash transactions typically close in 10–14 days, compared to 30–45 days for financed deals. Some buyers close in as few as five days depending on the seller's timeline.

Why are investor cash offers lower than market value?

Investors price offers to cover repair costs, carrying costs, and their required profit margin. An offer below market value often reflects the renovation budget the investor absorbs so the seller does not have to.

How do I verify a cash buyer is legitimate?

Request a verified bank statement or an official letter from a financial institution. Check the buyer's history of completed transactions and ask for references from past sellers in your area.

Is selling to a cash investor worth it?

For homeowners facing foreclosure, owning a repair-heavy property, or needing a fast relocation, a cash offer delivers certainty and speed that a traditional sale cannot match. The lower price is often offset by savings on repairs, commissions, and carrying costs during a longer listing period.